Readers of this blog would know that I got 8 lots of HPH at IPO from bidding 11 lots.

The issue price is USD 1.01 but debuted at USD 0.96. I sold 6 lots at USD 0.95 and 2 lots at USD 0.92.

The most amazing thing about this was this. I told my colleague that I was wrong

- to not avoid this stock as my skill in discerning good stock from bad stock is not good.

- I should have kept this 8 lots and not sell at a loss. Taking a USD 700 loss is not right.

This stock have haunt me for quite a while and with this volatility in this market, I feel I should revisit this.

Profits, Free Cash Flow

The consensus profits estimate is around HKD 2100 mil.

Operating Cash Flow is estimated to be HKD 5390 mil.

Capex for the first year is estimated to be HKD 2000 mil, which will go down subsequently to HKD 1000 mil.

Capex seem to be able to meet deprecation of HKD 2700 mil in the first year but after that, analyst expect it to go down. What does that mean? does HPH start self liquidating?

Overall, we can expect free cash flow to come in at HKD 3390 mil, or HKD 4100 mil subsequently.

To pay out USD 0.06, HPH needs HKD 4100 mil, which the free cash flow should barely suffice.

Current Projected Dividend Yield at 10%, Earnings Yield at 5%

The consensus projected full year dividend per share is USD 0.06 to USD 0.07. At current price of USD 0.62, the yield is about 9.6% to 11%.

That looks a pretty decent yield, but the caveat is that a lot of how much HPH yields depends a lot on the amount of traffic handled by the ports.

In a downturn, it is likely the traffic will fall, income will fall and so will earnings. Although, the traffic will not fall as badly as ship charterers, it will still affect the yield.

The caveat as well, is that although dividend yield is 10%, free cash flow yield is 10%, earnings yield is just half that at 5% and not looking to increase.

The reason for the big difference is due to depreciation and changes in capital expenditure. I truly believe that this trust is self liquidating, meaning that at the end of the concession period, HPH could not operate the trust again to earn if they do not ask for more money from the investors.

Concession Period

I summarize the concession periods of HPH’s current port assets:

HITL and COSCO-HIT

Land Area: 141 HA

Concession Expire in 2047

Yan Tian West Port Phase II

Land Area: 44 HA

Concession Expire in 2038

Yan Tian Phase I&II

Land Area: 130 HA

Concession Expire in 2043

Yan Tian Phase III

Land Area: 226 HA

Concession Expire in 2052

Yan Tian West Port Phase I

Land Area: 17 HA

Concession Expire in 2055

To make calculations easier later, the average concession life of HPH’s total assets is 36 years.

Net Debt to Asset 16%, ROA 1.44%

I think in terms of leverage, HPH is in a good position. The trend for these trusts seem to be light on debts and let the equity investors take the risks.

ROA is very low at 1.44%, I have yet to find out why it is so low.

Price Earnings 19 times, Price to Sales 3.46 times, Price to Book 0.44 times

The cherry picking ratio out of all these valuation ratio is the price to book at 0.44 times. Now I do feel that this might be even more dangerous since if they are paying out dividends through depreciation, it would mean that book value will continue to go down. So what is the true book value? I think using book value as an estimate is not really accurate here.

A PE of 19 times means its likely you will earn your money back in 19 years. The concession of their assets should last for 36 years. Is it undervalued? If I compare to other utilities such as Singtel or REITs their PE currently is less than 12-14. HPH looks expensive right here.

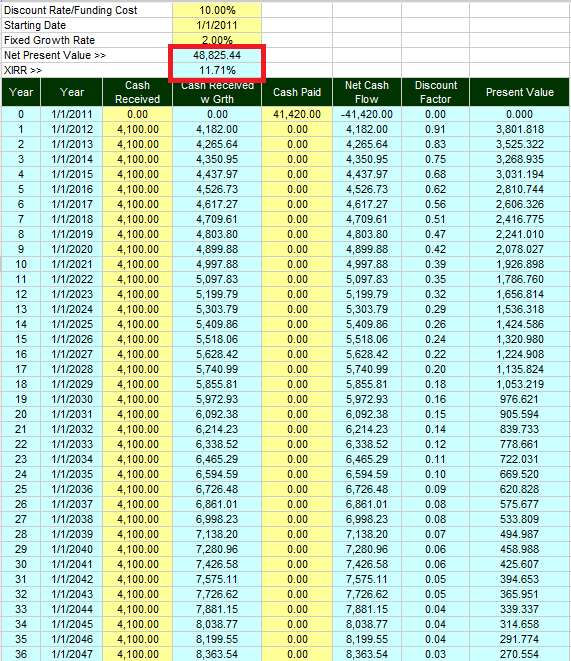

Discounted Cash Flow and XIRR Valuation

Now we know that the concession to operate the ports last till 2047 on average. This gives HPH a current operating duration of 36 years at most.

We know that the current dividend yield and free cash flow yield 10% requires a payout of HKD 4100 mil and since dividend payout equals to free cash flow and that this is far higher than net income earnings, HPH will end up with zero net assets at then end of this 36 years.

We carried out a discounted cash flow estimation using our Investment Moats Calculator.

There are 2 ways to derive the valuation but they should end up at the same place.

We input HKD 41420 mil which is the current market cap (USD 0.62) into year zero cash flow.

For every year up till 2047 we received HKD 4100 mil, which equates to the free cash flow.

The cash flow received will grow at a long term growth rate of 2%.

The XIRR, or the rate or return is 11.71%, which almost equates to the free cash flow yield currently.

The second method is instead of using XIRR we use a discount rate of the kind of required rate of return we demand. Based on the risk, we use a discount rate of 10%.

The end state is that we arrive to a Net Present Value of HKD 48825 mil, which is more than the current valuation.

It would seem that based on our cash flow estimation, HPH is fairly value now. However, should you buy it at current price there isn’t much margin of safety there.

Price Chart

This price charts looks like a mirror image of CitySpring’s price chart. For those not familiar with Cityspring, Temasek IPOed this utility trust at SGD 1.50 and since then it have been dropping to SGD 0.39.

I sort of have a feeling for these business trust you should NEVER EVER get them at IPO because they are NEVER going to be worth it.

Seems like I need case studies like this to drive it into my thick skull.

The drawdown should you are still holding to this stock is 40%. My loss instead of a USD 640 loss would have been, USD 3,200.

Conclusion

Sometimes there is never a right or wrong answer to things. Cutting loss works for some people, doesn’t work for others. Some people feel entirely comfortable with averaging down value investments.

To me, there is a limit to my valuation abilities and there are certain factors that I cannot account for even with all the due diligence that I have carried out.

The decision to cut looks to be the right one, even though I relied on my gut. But really, you developed a gut feel when you get more experience and somehow information gets processed in a unique way you cannot fathom.

To me, gut feel nowadays is a sub conscious analysis of whether I made a right purchase or not.

At current valuation, HPH looks to be approaching fair value if not abit under value.

As a business, this trust will generate income through bad times, but traffic is likely to fluctuate. It is likely it will not be a going concern, given that its net debt to asset is only 16%.

The return to maturity of this asset looks to be 10%, the caveat being that long term free cash flow fluctuates around HKD 4100 mil, for that to happen traffic and margins must fluctuate around this.

In a bear market, cheap things can get cheaper and I am satisfied I get a rough estimation of the value of this trust. Should it go into deep discount, I may look to pick up HPH.

I run a free Singapore Dividend Stock Tracker . It contains Singapore’s top dividend stocks both blue chip and high yield stock that are great for high yield investing. Do follow my Dividend Stock Tracker which is updated nightly here.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

Albert

Tuesday 13th of March 2012

I also purchased this REIT at IPO and the price has tumbled and recovered a bit now at US$0.77. But the dividend yield was only about 7%. Should I wait and wait until I recoup all my investments? That would be at least 5 years?

Drizzt

Thursday 15th of March 2012

Hi Albert at current price i think 3 years of divy should earn u back. but the question long term wise is do u see this as a capital asset that can earn a better return than the alternative should you switch out of this?

agnes

Thursday 26th of January 2012

you sold at the right time, i bought it at IPO too, and i reckon the price has dropped by 40%?

Drizzt

Friday 27th of January 2012

hi agnes, its really unfortunate really. the lesson learn is that IPOs cut both ways. this is an example of us putting too much faith in Li KarShing.

YT

Tuesday 29th of November 2011

Hi Drizzt,

Thank you for your advice. Sorry to hear your investment MIIF.

I will hold on to the 10 lot for the time and to get the dividend next year and see how it goes but really make a stupid mistake to buy 10 lots. If to cut loss, would be US4k, that would be unbearable. But if patience running out eventually....

My worry is HPH could go down further next year, but just hope for the dividend to make up for the loss.

Drizzt

Monday 28th of November 2011

hi YT, i am sorry to hear that. I got in a worse situation when i got 8 lots at IPO when i really don't want so much. I cut 6 at your price.

if you hold it the dividend will come during the dividend cycle. don't worry about that.

but many would have advised you to hold on when it will eventually go up.

the rational why i cut was that, the allotment and price movement indicates to me that the price of 1.01 is an overpriced amount for the stream of cash flows that i am paying for, factoring the risk.

and i do not see a good reason why i should hold something with an inflated price tag. on hindsight it was a good call.

the decision for you now is that you have held on for it for some time. whats going through your mind is whether you should cut it. this mirrors very closely to my decision to cut my MIIF which i bought at $1.20 and it was languishing at $0.48. You are probably looking for a psychological relief.

Evaluate, based on our posting (not just my point of view!) and quantifiable figures whether HPH will be a going concern and whether it can still be a viable business.

if it is, what is the fair price to pay for it? is 60 cents now a fair or discounted value? Will it make sense for me to accumulate more or is this a total dud?

if its a total dud, then perhaps you should cut it. if its not then at a low price it presents a good investment.

mind you, my MIIF example went down to as low as 23 cents. although i had a very bad experience with it, i am still evaluating it together with another stock that went down from 1 dollar to 16 cents.

https://investmentmoats.com/money-management/dividend-investing/macquarie-international-infrastructure-fund-miif-q3-2011-and-9-month-results-8-yield-locked-in/

In investing, we need to put our emotion aside and evaluate rationally.

had u bought MIIF at 23 cents and base on the declared yield of 4 cents or 5.5 cents, its a 17% yield or 24% yield! you can practically earn back ur capital in 4-5 years plus capital appreciation.

evaluate whether the management is worth to give more time.

YT

Sunday 20th of November 2011

I bought 10 lot HPH Trust at 0.965 and still holding on to it. Am lost what to do, and seems there is no dividend for the period Jul to Sep 2011.